MENA Energy Recap, Q1 2025: Tariffs and Sanctions Loom Large as Trump Returns

The MENA Energy Recap is a quarterly review of key energy developments that took place in the Middle East and North Africa region from January to March 2025 and what they signal for the months ahead. The recap views these developments through the lenses of policy and strategy, energy security, and markets.

Q1 2025 in Brief

With the first week of April now firmly in the rear-view mirror, the first quarter of 2025 can easily be characterized as a period of scene-setting for what looks likely to be a highly volatile year in both markets and geopolitics, with the latter weighing heavily on the former. The region’s major hydrocarbon producers may face greater fiscal and economic challenges this year than initially expected, due to oil prices potentially taking a hit from worldwide trade tensions and efforts by the Organization of Petroleum Exporting Countries plus 10 non-OPEC oil-producing nations (OPEC+) to bring undisciplined producers under control.

While most producers will largely escape the direct impact of the tariff policy implemented by President Donald Trump’s second administration, the indirect effects of tariffs on major oil- and natural gas-consuming economies are another matter entirely. For MENA economies that are net consumers of energy, geopolitical tensions will remain a key issue to watch as energy security continues to be a concern in the months leading up to summer. This may be due to difficulties with procuring energy imports or the relative ability to attract investment into domestic energy production in a potentially riskier investment climate.

For OPEC+, the Trump Factor Will Remain Present through 2025

-

OPEC+’s decision to unwind its voluntary production cuts — one of three layers of deep cuts it has maintained since late 2022 — came as a surprise to many market-watchers despite having been a part of the group’s plans since the end of last year.

-

The group unveiled another upset to its plans on April 3 with the decision to boost supply by 411,000 barrels per day (bpd) from May, equivalent to three months of supply additions under the plan it had agreed to just one month prior.

-

The timing of its decision is hard to ignore. Not only did it announce the production ramp up in the immediate aftermath of the unveiling of a sweeping set of tariffs by the White House on April 2, but the decision comes in advance of Trump’s first planned trip to the Gulf region, where he is expected to visit OPEC+ leader Saudi Arabia and the United Arab Emirates, another powerful member state.

Outlook: The process of returning to the market some 2.2 million bpd worth of production cuts was delayed multiple times last year and proceeds under extremely tenuous circumstances. Although the policies of the United States do not represent the sole set of factors determining how the group will implement its market balancing strategy, these variables will be front and center for at least the first half of the year, if not longer.

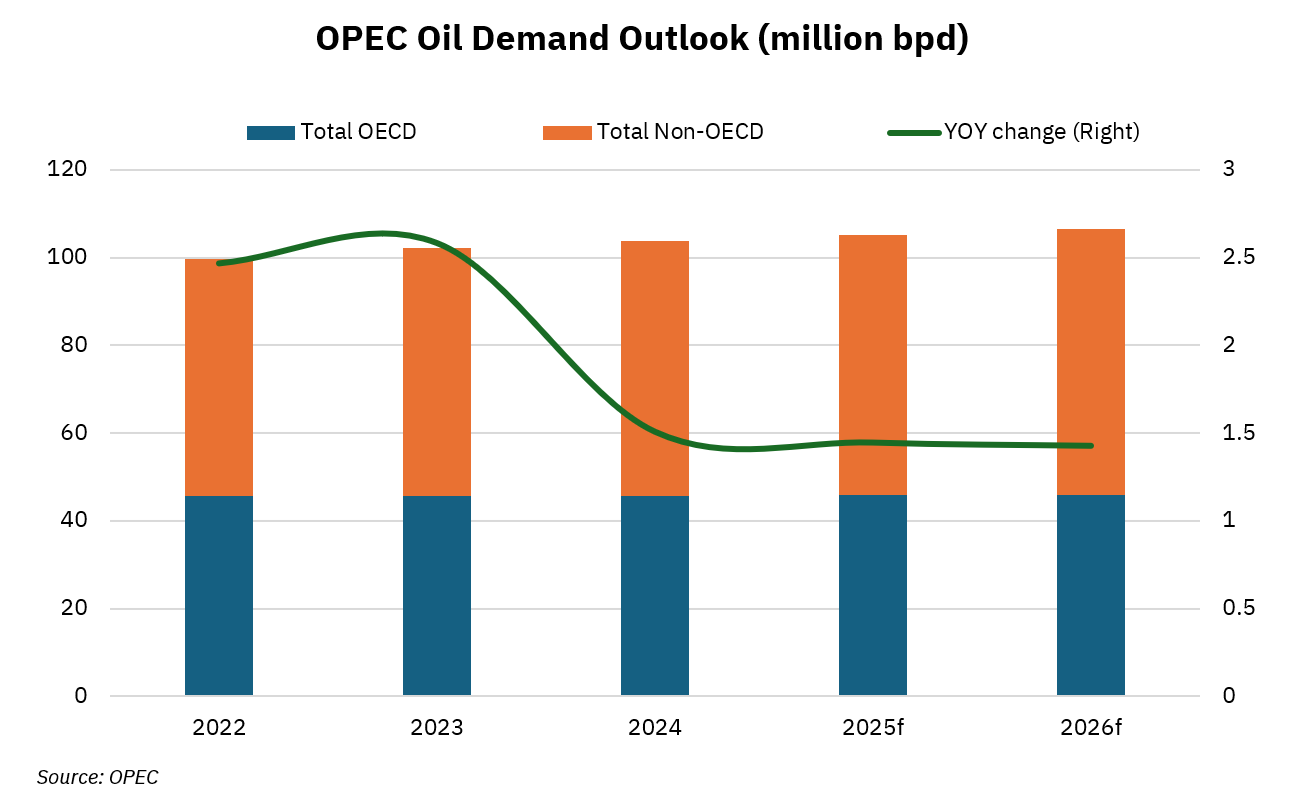

OPEC’s internal oil demand forecast, which, most analysts would argue, typically leans toward a bullish outlook, has seen demand growth decline toward the middle of the current decade. So there is perhaps some irony in the announcement of even more supply additions subsequent to “Liberation Day,” the term the White House chose for the rollout of its anxiously awaited tariff package. The Trump administration’s mercurial approach to the use of tariffs has roiled equity markets and left the industrial and other sectors in both the US and abroad unsure of how to react to the drastic actions. OPEC+’s announcement quickly sent benchmark oil prices below $70 per barrel and into a price range with which few of its members will be pleased.

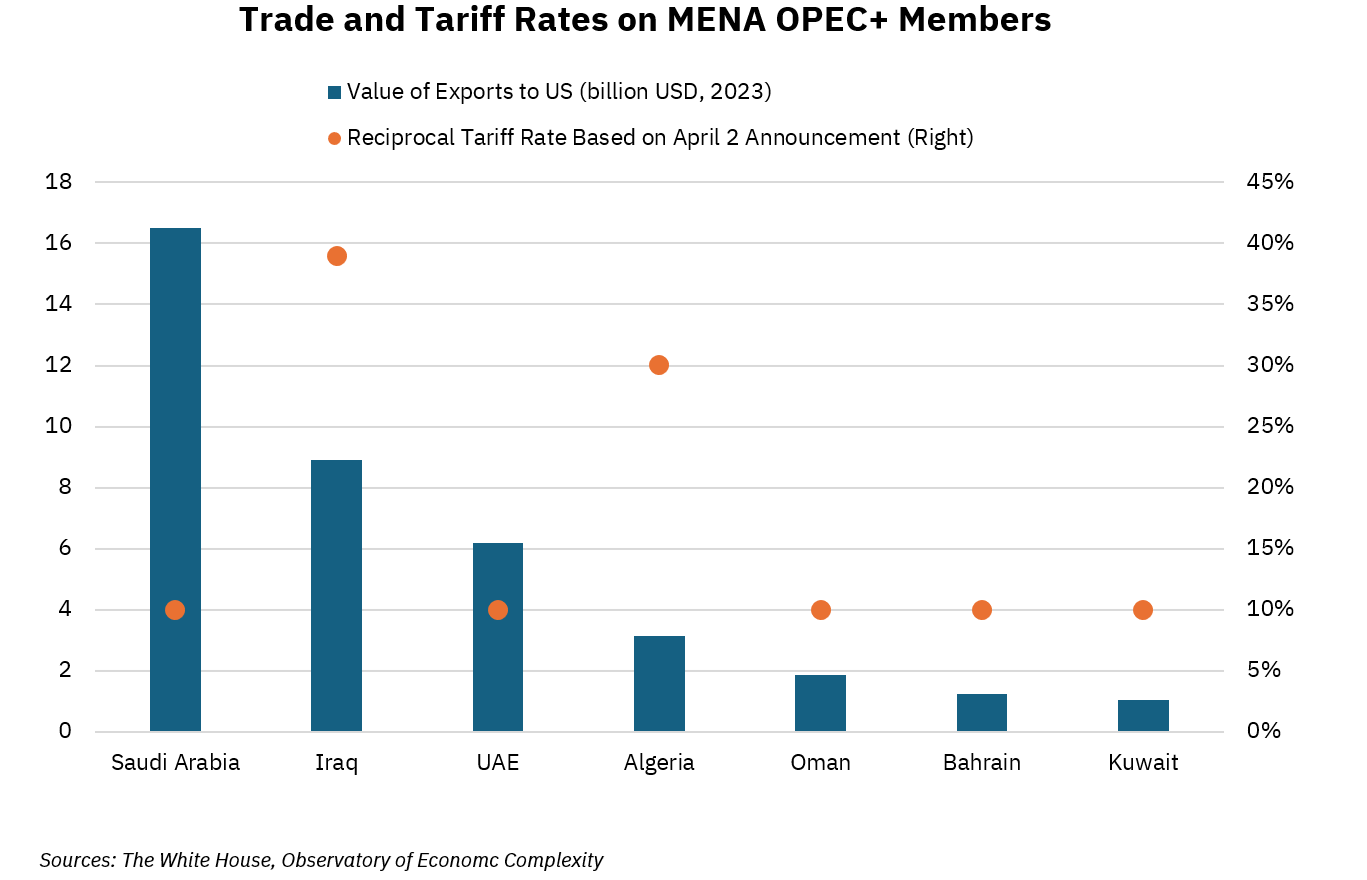

For OPEC+, a key concern will be potentially corrosive effects on oil demand, particularly in Asian economies with high exports to the US. An economic slowdown in Asia would hold extremely bearish prospects for oil markets, but confusing messaging in the run-up to “Liberation Day” has only clouded this outlook. Accordingly, tariffs may be one of the most impactful policies on OPEC+ strategy and oil-dependent MENA economics for much of the coming year. Additionally, a number of OPEC+ members have found themselves in the crosshairs of Trump’s reciprocal tariff policy and likely see a production increase, which would support the administration’s goal of lowering energy prices, as an initial olive branch toward relief from these measures. With the exception of Bahrain, all of the MENA region OPEC+ producers that will commit to a further production increase in May were hit with at least 10% reciprocal tariffs, while Iraq and Algeria received rates of 39% and 30%, respectively.

Yet the volatility does not stop there. The Trump administration’s policies toward three of OPEC+’s members, Russia, Iran, and Venezuela, will affect the group’s ability to unwind its production cuts. Washington’s push to secure a peace agreement for Russia’s war in Ukraine is sure to contain some element of sanctions relief for Moscow, which could see a considerable number of Russian barrels return to the market. Simultaneously, a return to the “maximum pressure” campaign against Iran will likely see the removal of Iranian barrels. The group’s plans to unwind in April will be a source of relief should a large volume of Iranian supply disappear, since OPEC+ is averse to filling gaps in the market created by sanctions on its own members. However, Washington appears keen on a new agreement with Iran, which may only inject more volatility into the supply side of the market if a deal tied to sanctions relief can be reached faster than expected.

Gulf Investment in US Energy, Especially LNG, Looks Set for Another Wave

-

While the Trump administration has stated that it plans to boost US oil and gas production as a key component of its energy policy, American production is already at an all-time high, raising questions as to how much the president can actually do to increase output.

-

However, an energy policy agenda that shows significantly greater favor to fossil fuel growth is likely to support continued expansion of the US liquefied natural gas (LNG) industry, which faced a key setback under the administration of President Joe Biden in the form of a pause on approvals for projects with exports headed to non-free trade agreement (FTA) countries.

-

Gulf national oil companies (NOCs) made major investments in US LNG during 2024 and are clearly signaling an intent to continue investing in US gas and LNG under the Trump administration, which had previously welcomed Gulf investments in the US.

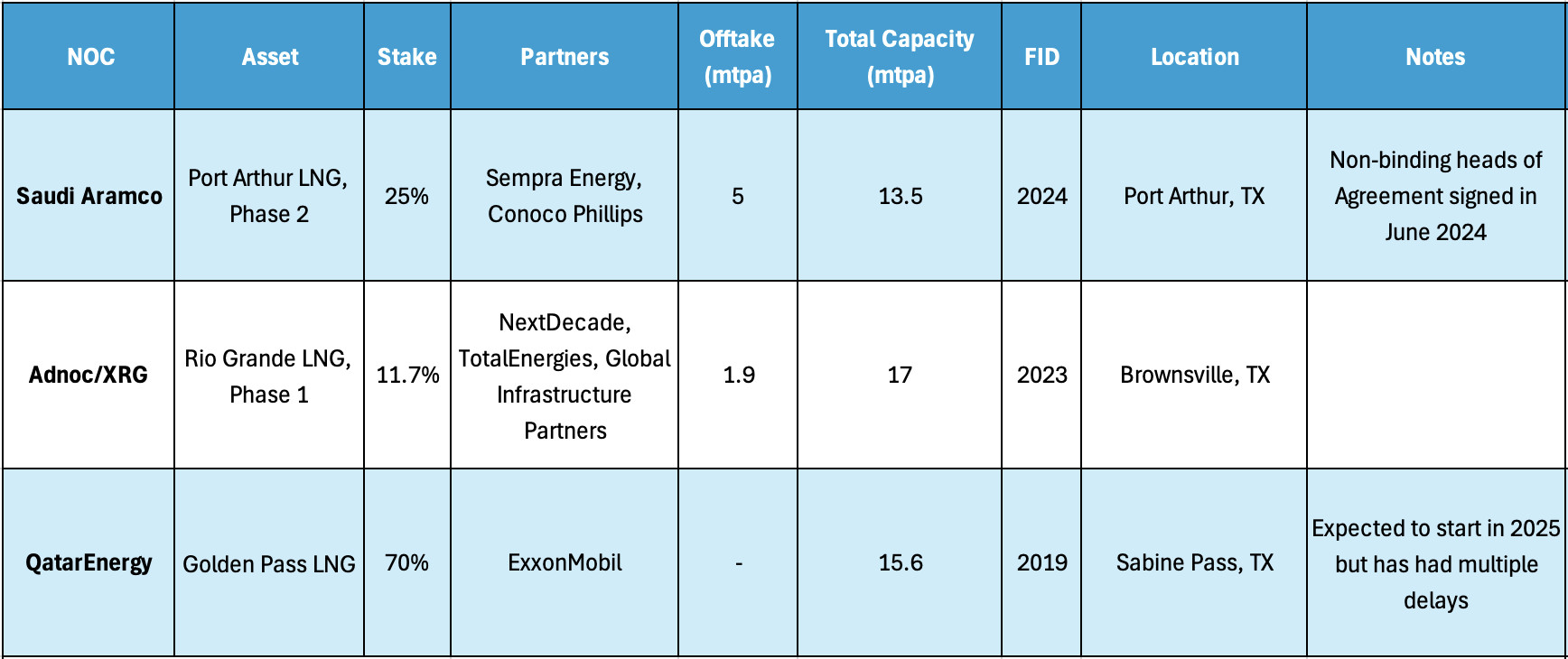

Outlook: Gulf producers view the US energy sector as an opportunity. All three major NOCs from the region — Saudi Aramco, Abu Dhabi National Oil Company (ADNOC), and QatarEnergy — are investors in the US LNG sector. Saudi Aramco and ADNOC are more limited in their ability to establish or grow LNG export capacity in their home countries; as a result, overseas investment has emerged as a preferred strategy for gaining exposure to gas markets.

Gulf firms are no strangers to investment in the US energy sector. The largest refinery in the US, Motiva, is a wholly owned subsidiary of Saudi Aramco. However, QatarEnergy’s presence on the US Gulf Coast, where it partners with US supermajor ExxonMobil via its 15.6 million-ton-per-year (mtpa) Golden Pass LNG project, is a prime example of “diplomacy by investment.” Its presence grew when it signed an agreement for the Golden Triangle petrochemicals project in 2019 during Qatari Emir Tamim bin Hamad Al Thani’s visit to the Trump White House the same year, with both leaders in attendance for a signing ceremony. While Gulf leaders have long been aware that investment is among the most direct ways to remain in the good graces of the Trump administration, energy investments were less prolific during Trump’s first term, a dynamic that looks likely to change during his second.

Table 1: US LNG Investment

To be sure, maintaining strong ties with the Trump administration is not the only driving force behind this investment pattern. In 2024, a new wave of Gulf LNG investments materialized. Both Aramco and ADNOC took direct equity stakes in individual operations and signed agreements for offtake from US-based projects, which essentially resulted in a long-term agreement to buy volumes of gas from specific LNG plants that the firms will then resell elsewhere in the world. With the Trump administration clearly favorable to both the oil and gas sector as well as countries making large-scale investments in the US, American gas assets present fewer near-term risks than they would have in the recent past and are viewed as even more attractive by Gulf NOCs than they were just last year. Initial expectations for 2025 point toward another Aramco entry into US LNG, with Australia-based Woodside Energy’s Louisiana LNG its likely target; any deal would likely make up part of Saudi Crown Prince Mohammed bin Salman’s $600 billion US investment pledge. After ADNOC head Sultan Ahmed al-Jaber professed his desire to “make energy investment great again” during CERAWeek in March, he held several notable meetings during a subsequent trip to Washington, where he met with US senators from Alaska, Utah, and Pennsylvania. These meetings may provide early clues as to where ADNOC’s newly minted XRG subsidiary, which is charged with managing the firm’s growing international portfolio, may seek to invest in the US after Jaber expressed his intent to acquire new assets along the natural gas value chain. Jaber also serves as the chair of UAE state renewables champion Masdar, which is increasing its US holdings as well. Under the current administration, though, XRG is more likely to serve as the vehicle for the UAE’s expanding US energy portfolio.

Russia, Qatar Step in as Sanctions Complicate Syrian Energy Procurement

-

Improvements in Syria’s internal cohesion have enabled Damascus to resume purchases of oil and gas from the energy-producing heartland of its northeastern region.

-

However, this has not eliminated the need to procure energy from external sources. According to figures from shipping data firm Kpler, Syria has imported around 2.6 million barrels of crude oil and refined products in 2025. Critically, most of these deliveries have arrived on Russian vessels subject to US sanctions that make up the so-called “dark fleet.”

-

Meanwhile, Qatar agreed to supply Syria with natural gas on March 13. The gas will likely be delivered via a floating storage and regasification unit (FSRU) in southern Jordan, where it will then be transferred on to Syria via pipeline.

Outlook: Syrian energy security is fragile and in dire need of sanctions relief to enable Damascus to import oil and gas in the near term, while seeking investment to rehabilitate its beleaguered energy sector in the long term. This would allow interested parties to return to the country and unlock investment needed to increase domestic energy output and repair or upgrade its aging refineries at Banias and Homs. The same applies to potential investors in solar power generation projects, although given the fact that much of Syria’s power generation capacity actually survived the conflict, investment in its transmission and distribution infrastructure is likely to be a higher near-term priority.

However, Damascus’ turn to sanctioned Russian suppliers for oil imports highlights just how constrained this process may be by US and European sanctions. The Banias Refinery in January issued a tender for around 3 million bpd in crude oil imports in addition to smaller volumes of refined products like gasoline and fuel oil. While officials eventually disclosed that an award had been made, the supplier was not disclosed and it was widely believed that sanctions risks deterred potential bidders. Despite Europe’s push for greater sanctions relief on Damascus and the US Treasury Department’s issuance of General License 24 in January, the risk of falling afoul of US sanctions and potential concerns about the new government’s ability to finance these deals clearly outweighed any potential benefits of engaging in energy transactions with the new government.

Lagging efforts to enable Syria to import energy from the broader market not only risk replacing its previous dependency on Iranian barrels with Russian ones, but have also at times forced Syrians to turn to smugglers that import fuel from neighboring Lebanon. This is not only a poor means of shoring up energy security; it is also not conducive to advancing a sustainable reconstruction process. Still, some positive developments have taken place in the interim. In mid-March, the Qatar Fund for Development announced an initiative that will supply gas to Syria via neighboring Jordan. Curiously, the announcement does not reveal exactly how the gas will be delivered, only indicating that these volumes would enable the provision of 400 additional megawatts of power per day. While any gas transiting Jordan would need to be imported via an FSRU at Aqaba, it is unclear if Qatari volumes will resume transiting the Red Sea in what would be a considerable show of support from Doha, or if Qatar will simply provide financial support for LNG purchases. In either case, the arrangement reportedly received tacit approval from Washington, hopefully indicating some level of awareness of the risks incurred by neglecting Syria’s energy future.

Aramco’s Revised Blue Ammonia Goal Signals Trouble for Clean Hydrogen

-

In March, Saudi Aramco slashed its production targets for blue ammonia — produced by combining nitrogen from air with hydrogen sourced from natural gas and capturing and storing the byproduct carbon — from 11 to 2.5 mtpa by 2030, in a move that represents a highly bearish outlook for the development of clean hydrogen/ammonia markets.

-

The Saudi oil and gas firm had previously aimed to produce 11 mtpa by 2030, a target that was unmatched by regional peers. Its revised goal still exceeds the capacity of flagship blue ammonia projects under construction by regional peers ADNOC and QatarEnergy.

-

Aramco was poised to emerge as a major low-cost producer of the clean fuel. The fact that it has changed course on its approach to what was not long ago regarded as a market with major growth potential is likely an indication that the road ahead for other aspiring producers will be tough.

Outlook: The Saudi NOC’s decision to retool its hydrogen strategy was likely a long time coming. Blue hydrogen is produced using a process called steam methane reforming (SMR), in which natural gas is the main feedstock and carbon capture and storage (CCS) capacity is used to abate the emissions associated with the SMR process, thus rendering it a low-carbon form of production. Any firm investing in blue hydrogen production requires a reliable and cost-effective source of natural gas, and the ability to invest in the capital-intensive task of building CCS capacity. Aramco has long held the former, and while it plans to invest billions in growing its CCS capacity, CEO Amin Nasser cited a lack of buyers as a key reason for the decision, asserting that the market for blue hydrogen simply is not developing at a rate that justifies such high levels of investment. This is unlikely to bode well for the development of the clean hydrogen market.

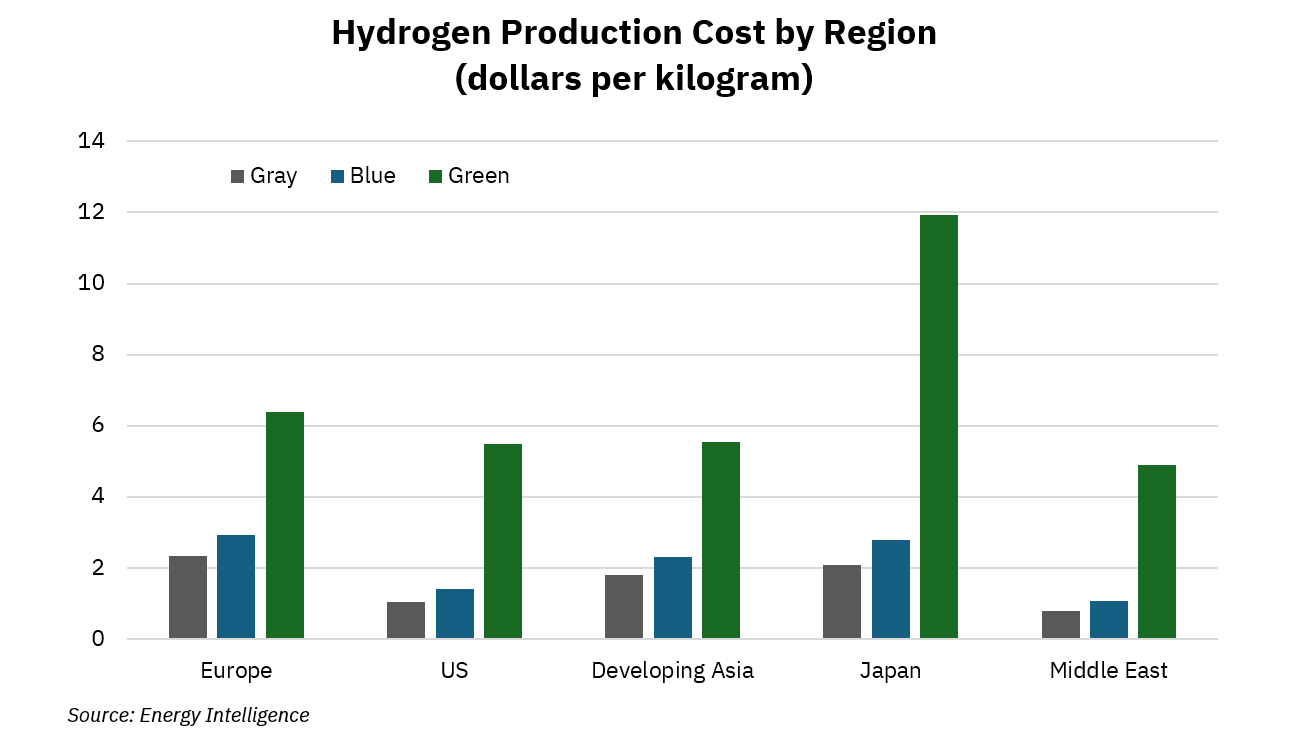

The slow development of a market for clean hydrogen, which had seen considerable enthusiasm in the early 2020s, holds implications for the region beyond Saudi Arabia. A number of hydrogen and ammonia projects — of both the blue and green variety — are under construction in the UAE, Qatar, Oman, Saudi Arabia, Egypt, Morocco, and others. Much of the region boasts low-cost renewable power generation potential required for green hydrogen production, which splits water molecules into hydrogen and oxygen gas using electrolysis powered by clean (such as wind or solar) energy. The Gulf states also hold large reserves of low-cost natural gas, increasing its viability as a blue hydrogen feedstock. Yet the supply-side potential of the region represents only half of the clean hydrogen puzzle without congruent growth in global demand. The International Energy Agency (IEA) provided a condensed picture of this dilemma in its late 2024 Global Hydrogen Review. Where worldwide “policies and targets” for hydrogen demand add up to just 11 million tons by 2030, production targets stand at 49 million tons by the same year. In essence, there is no shortage of prospective hydrogen producers interested in leveraging their competitive advantages, but those interested in consuming their output are much fewer and further between.

At the core of clean hydrogen’s demand problem is its affordability. Existing demand is concentrated in select industrial applications such as oil refining and the production of chemicals and metals. These rely overwhelmingly on gray hydrogen, mostly produced from natural gas whose emissions are unabated. While less environmentally friendly, gray hydrogen is much cheaper to produce and therefore more cost competitive than its low-carbon counterpart.

What then does this mean for would-be clean hydrogen producers in the MENA region? Some projects have already found off-takers for their upcoming production; but in the near term, it appears increasingly possible that countries targeting huge volumes of clean hydrogen or ammonia for export may find themselves competing for a market that is smaller than expected. Others may look toward the development of local markets, where low-carbon hydrogen production holds the potential to be a low-cost solution, rather than one that adds costs. Morocco provides a strong example of this dynamic, as its green hydrogen strategy targets exports to Europe, but is also crafted to meet domestic needs such as offsetting ammonia imports.

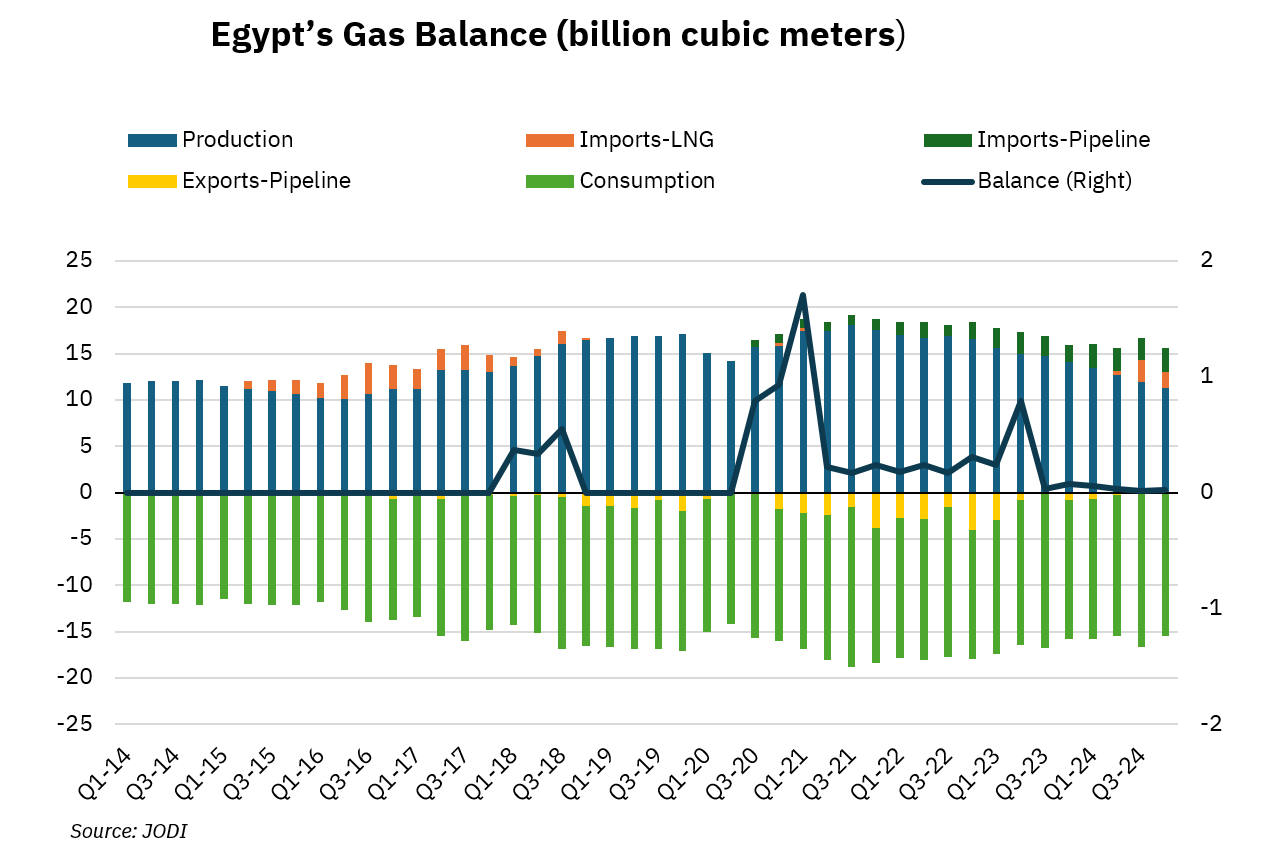

Egyptian Gas Output Continues Collapse, With No End in Sight

-

Cairo continued to experience shortfalls in its natural gas supply in 2024, the direct result of which was an inability to meet key energy demands for households and industry alike. Rolling blackouts peaked during the hot summer months, but the structural factors that led to ongoing shortages remain firmly in place.

-

Egypt’s heavy reliance on natural gas as a source of energy has placed its domestic sources of production under heavy strain. Ongoing exploration efforts by international oil companies (IOCs) have yielded some new discoveries, but fast-tracking new supply faces multiple challenges.

-

Insufficient gas supply forced Egypt to swing from being an LNG exporter at the outset of the year to again becoming an importer. LNG will further add to its gas import bill, as pipeline gas from Israel has proved a lifeline for Cairo, despite increased volumes still proving insufficient to keep the lights on.

Outlook: The ongoing Egyptian energy crisis, which closely resembles the shortages the country endured in the early 2010s, may ease in 2025, but expensive energy imports will present both the state and economy with major added costs. As LNG is sold in US dollars, imported gas is considerably more expensive than domestic production or nearby pipeline supply and will cause a further drain on Egyptian finances at a time when Cairo can ill afford it.

Egypt cannot end its energy shortfalls by simply increasing domestic production. New gas discoveries or increases to existing output pose significant challenges for IOCs operating in Egypt, where gas reservoirs are notorious for high decline rates, and Cairo has developed a habit of letting payments to IOCs periodically fall into arrears. Where Egypt’s balance of natural gas supply and demand is in deficit, so too is the balance of trust between many of its IOC operators and their state-backed partners. Egypt boasts a collection of upstream heavy-hitters that would be the envy of any country seeking IOC investment: Eni, Shell, ExxonMobil, and BP-ADNOC joint venture Arcius Energy all hold numerous assets in the country, to name a few. Yet with both fiscal and economic crises that show few signs of subsiding, Cairo has little maneuverability to enact measures like improvements in IOC operating terms that would potentially incentivize greater investment.

What differentiates Egypt’s more recent crisis from its position in the past is that it has begun to accumulate an impressive pipeline of renewable energy projects that continue to successfully secure financing. As this array of new solar and wind projects begins to operate, it will gradually reduce the Egyptian power sector’s dependence on natural gas and ostensibly help ease the strain that the country’s rapidly growing demand has placed on both its gas resources and finances. Yet these projects do not present an overnight solution for Egypt’s energy woes. Imports of LNG and Israeli pipeline gas may improve the Egyptian gas balance enough to avoid major power outages this summer. But where citizens can be shielded from the heat, Egypt’s finances will not be.

Outlook for Q2 2025

The first quarter of 2025 has been a reminder that the impact of US policy remains incredibly significant for the energy landscape of the MENA region, whether it comes to energy, trade, or foreign policy. This will continue into the second quarter and beyond as both tariffs and sanctions play their part in markets and policymakers around the world scramble to respond.

Yet outside of the potential impact that tariffs will have on oil demand, sanctions will remain the key policy tool affecting the region’s energy industry and markets, whether this effect is felt directly or indirectly. It is unlikely that any sector in the MENA region, perhaps with the exception of the financial sector, has so directly felt the impact of US sanctions as the energy industry. This is not only for the effect that sanctions have had on the oil trade but for impacts on other forms of energy production and security in a region where, as almost everywhere else, energy is inherently political.

In Iraq, reliance on gas and power imports from neighboring Iran has long been tolerated by successive US administrations (including the first Trump White House). Blackouts have become a regular feature of life when heat reaches deadly levels, but Washington’s move to end waivers that allowed these imports leaves Baghdad with few alternative sources of supply, and certainly none that it can procure quickly. Likewise, as mentioned above, Syria’s options for badly needed energy imports are constrained by the mountain of US sanctions that its previous government accumulated during the country’s civil war.

Renewed engagement between the US and Iran could prove to be the most consequential policy outcome of all, should the two countries actually make headway in talks. While it is far from clear what the final version of a renewed nuclear agreement with Iran might look like, it is an absolute certainty that any such accord would include sanctions relief for Iran’s oil exports. With China currently the only buyer of Iranian oil, sanctions relief would see Iranian barrels return to market en masse, pushing down prices and creating headaches from Riyadh to Houston. Tehran has a track record of rebuffing attempts to discuss assignment of a new OPEC production quota (from which it is currently exempt), and there is little reason to think that its stance has changed recently.

While the second quarter is unlikely to see major progress on this front, if any is to be achieved at all, near-term risks to the regional energy trade may flare up in the interim. Should the US move to aggressively enforce sanctions on Iran by pursuing measures such as seizing tankers, then new disruptions to shipping in the Strait of Hormuz and Gulf of Oman may emerge, similar to those seen in 2019, when tensions ran high. Few fears currently point toward major oil supply outages in the region; but as most of OPEC+’s more than 5 million bpd in spare capacity is located in the Gulf, any spike in regional tensions will have a commensurate impact on benchmark oil prices.

Colby Connelly is a Senior Fellow at MEI. He is also a senior analyst at Energy Intelligence, where he works with the firm’s research and advisory practices.

Top photo of Saudi oil platform on Chinese ship by Costfoto/NurPhoto via Getty Images

The Middle East Institute (MEI) is an independent, non-partisan, non-for-profit, educational organization. It does not engage in advocacy and its scholars’ opinions are their own. MEI welcomes financial donations, but retains sole editorial control over its work and its publications reflect only the authors’ views. For a listing of MEI donors, please click here.

Distribution channels: Politics

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

Submit your press release